Alright, let’s talk about something that often gets a bit of a dusty reputation: life insurance. Specifically, we’re diving into life insurance for over 50 UK guaranteed acceptance. Now, if you’re like many people, you might hear “guaranteed acceptance” and think, “Ah, the easy option,” or perhaps, “What’s the catch?” And honestly, both thoughts are pretty natural. But here’s the thing: for those of us navigating life over 50 in the UK, this particular type of policy isn’t just an ‘easy option’ – it’s a strategically significant one, and understanding why it matters is far more important than just knowing it exists.

I’ve seen countless individuals, friends, and even family members grapple with the complexities of securing financial peace of mind as they get older. The traditional routes, with their medical exams and lengthy health questionnaires, can become daunting, if not outright exclusionary. That’s where guaranteed acceptance life insurance steps in, but its true value isn’t just in its accessibility; it’s in what it represents for your future and the legacy you wish to leave.

Decoding “Guaranteed Acceptance” | What It Really Means for You

When an insurer says “guaranteed acceptance,” they mean it. This isn’t marketing fluff; it’s a fundamental promise. What it boils down to is this: if you’re a UK resident within the specified age range (typically 50-80 or 50-85, depending on the provider), you are guaranteed to be accepted for coverage. Full stop. No medical questions, no health checks, no intrusive probing into your medical history. This is perhaps the biggest differentiator, and it’s why terms like no medical exam life insurance UK are often used interchangeably.

Think about it: in a world where everything seems to require an assessment, a form, a deeper look, the simplicity of this is revolutionary for many. For someone who might have a pre-existing condition, or simply doesn’t want the hassle of medical underwriting, this is a game-changer. It opens the door to senior life insurance UK for a demographic that might otherwise feel excluded or overwhelmed by the process. It’s not just about getting cover; it’s about removing a significant barrier to entry, ensuring that more people can secure a degree of financial security for their loved ones.

I often hear people ask, “Is it truly no health questions?” And the answer is a resounding yes. This is the core principle of over 50s life insurance no health questions. The insurer takes on a broader risk pool, which, as we’ll discuss, comes with its own set of considerations, but the promise of guaranteed acceptance remains ironclad.

The “Why” Behind the “How” | The Hidden Value of Over 50s Life Insurance

So, we’ve established what it is. Now, let’s get to the why. Why would someone choose this specific path for their life insurance needs? It’s not always about dire health concerns, though that’s certainly a factor. Often, it’s about pragmatism, dignity, and a very human desire to not burden those we leave behind.

One of the most common drivers is the desire to cover funeral costs. Let’s be honest, funerals in the UK aren’t cheap. The average cost can be thousands of pounds, and for many families, that unexpected expense can be a significant strain during an already difficult time. A guaranteed acceptance policy can provide a lump sum that directly addresses this, ensuring your loved ones aren’t left scrambling. It’s a thoughtful act of planning, really, allowing them to grieve without the added stress of immediate financial pressure.

Beyond funeral expenses, many individuals use this type of policy to leave a small, thoughtful legacy. Perhaps it’s a modest gift for grandchildren, or a contribution to a spouse’s future. It might not be the massive payout of a traditional policy taken out in one’s younger years, but it’s a meaningful sum that can make a tangible difference. This is often structured as whole of life cover over 50, meaning it pays out whenever you pass away, not just within a specific term.

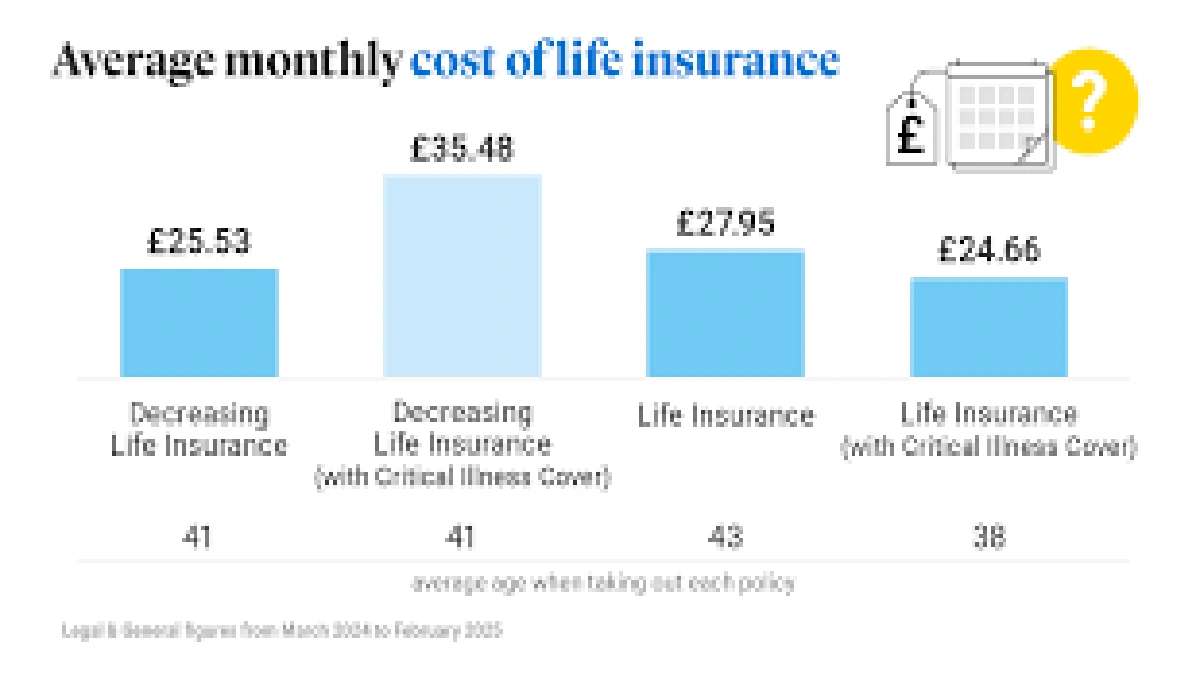

What fascinates me about this product is its underlying philosophy: it acknowledges that life is unpredictable, and that everyone, regardless of their health journey, deserves the opportunity to plan for their final expenses and leave a little something behind. And crucially, these policies often come with fixed premiums, meaning what you pay today is what you’ll pay tomorrow, providing budget certainty which is a huge relief in uncertain economic times. Understanding the cost of guaranteed acceptance life insurance involves balancing this certainty against the benefit amount.

Navigating the Nuances | What You Must Know Before Signing Up

Okay, so it sounds pretty good, right? Guaranteed acceptance, no medicals, fixed payments. But, as with anything in life, there are nuances, and understanding them is key to making an informed decision. This is where my “expert friend” hat really comes on, because I’ve seen people overlook these details.

The most important detail, and one you absolutely must be aware of, is the waiting period. Almost all guaranteed acceptance life insurance policies in the UK come with an initial waiting period, usually 12 or 24 months. If you pass away during this period (unless it’s due to an accident), your beneficiaries typically won’t receive the full payout. Instead, they’ll usually get back the premiums you’ve paid, sometimes with a small percentage added. It’s crucial to understand this, as it manages expectations. It’s a way for insurers to manage the risk associated with not asking health questions.

Another point to consider is the potential for premiums paid to exceed the benefit amount if you live a very long life. While the fixed premiums offer certainty, if you keep paying for many, many decades, the total amount you’ve contributed could eventually surpass the lump sum your beneficiaries receive. This isn’t a “catch” per se, but rather a characteristic of how this type of product is structured. It’s about peace of mind and immediate financial relief for your family, not necessarily a high-return investment. For those managing complex financial landscapes, understanding various insurance types, like evengeneral liability insurance, requires careful attention to detail.

Furthermore, it’s essential to compare providers. While the core promise of over 50s life insurance remains consistent, the exact benefit amounts, waiting periods, and any additional perks can vary. Don’t just jump at the first offer. Take the time to look at different policy details and read the small print. This isn’t just about the numbers; it’s about ensuring the policy aligns with your specific needs and expectations.

Beyond the Basics | Is it the Right Fit for Your UK Future?

So, who is this kind of policy truly ideal for? In my experience, it’s perfect for:

- Those with existing health conditions: If you’ve been turned down for traditional life insurance, or simply want to avoid the medical scrutiny, this is your straightforward path to cover.

- Individuals seeking simplicity: The process is incredibly simple. A few questions, a direct debit, and you’re covered. No fuss.

- Anyone primarily concerned with funeral plan insurance UK and immediate final expenses: If your main goal is to ensure your passing doesn’t create a financial burden for your family, this is highly effective.

- Those who value fixed premiums and budget certainty: Knowing exactly what you’ll pay each month can be a huge comfort.

However, it might not be the best fit if you’re in excellent health and looking for a very large sum of money to leave as a substantial inheritance. In such cases, traditional term life insurance or whole life policies with medical underwriting might offer a higher payout for the same premium, or a lower premium for a similar payout, simply because your risk profile is lower. It’s always worth exploring your options, perhaps by visiting resources likeMoneyHelperfor impartial advice.

The psychological comfort that comes with knowing you’ve taken care of things, that your loved ones won’t face additional stress during a difficult time, is immeasurable. It allows you to focus on living your life, knowing a crucial element of your future is managed. Just as knowing you have the rightfull coverage car insurancegives peace of mind on the road, guaranteed acceptance life insurance offers a similar sense of security for your family’s future.

Your Burning Questions About Over 50s Guaranteed Acceptance Life Insurance, Answered

Is guaranteed acceptance life insurance truly guaranteed?

Yes, absolutely. If you meet the age and residency criteria (typically 50-80 or 50-85 and a UK resident), you are guaranteed to be accepted for the policy, regardless of your health history or lifestyle. This is the core promise of this product.

What’s the catch with no medical questions?

The primary ‘catch’ (though I prefer to call it a feature) is the waiting period, usually 12 or 24 months. If you pass away from natural causes during this initial period, your beneficiaries typically receive a refund of premiums paid, not the full sum. Accidental death, however, is often covered from day one. This is how insurers manage the risk of not asking health questions.

Can I use this for funeral plan insurance UK?

Yes, many people specifically take out over 50s life insurance with guaranteed acceptance to cover their funeral expenses. The payout can be used by your beneficiaries for any purpose, including contributing towards or fully covering the cost of your funeral, easing the financial burden on your family.

Will my premiums increase?

Typically, no. Most guaranteed acceptance life insurance policies in the UK come with fixed premiums. This means the amount you pay each month will remain the same for the entire duration of the policy, providing predictable budgeting. Always confirm this in the policy details before signing up.

What if I change my mind?

You usually have a ‘cooling-off’ period (often 30 days) from when you receive your policy documents, during which you can cancel and receive a full refund of any premiums paid. After this, you can cancel at any time, but you won’t get back the premiums you’ve already paid, as the coverage would have been active during that time. For more information on life insurance regulations, you can check resources like theAssociation of British Insurers (ABI).

So, there you have it. Life insurance for over 50 UK guaranteed acceptance isn’t just a product; it’s a solution tailored for a specific stage of life, offering peace of mind when traditional options might feel out of reach. It’s about empowering you to make choices that protect your loved ones, ensuring that your legacy, no matter how big or small, is exactly as you intend it to be. It’s a powerful tool, when understood and used correctly, for continued financial security in your golden years.